Unlocking the Mystery: How Does Blockchain Work? A Beginner’s Guide to Understanding Distributed Ledgers

In an increasingly digital world, trust is a precious commodity. We rely on central authorities – banks, governments, social media giants – to manage our data, verify transactions, and maintain records. But what if there was a way to build trust directly into a system, without the need for a middleman? Enter blockchain, a revolutionary technology that is reshaping how we think about data, security, and transactions.

You’ve probably heard of blockchain in connection with cryptocurrencies like Bitcoin, but its potential stretches far beyond digital money. At its core, blockchain is a distributed ledger technology (DLT) – a fancy term for a shared, immutable, and constantly updated record book. But how does this digital marvel actually function?

This comprehensive guide will demystify blockchain, breaking down its intricate workings into easy-to-understand concepts, perfect for beginners eager to grasp this transformative technology.

What Exactly is Blockchain? The Digital Ledger Analogy

Imagine a traditional ledger, like a company’s accounting book. It records every transaction, one after another. Now, imagine if instead of just one person or company holding that book, millions of people around the world each had an identical copy. Every time a new transaction occurs, it’s added to everyone’s copy simultaneously, and once it’s written down, it can never be erased or altered.

That’s the simplest way to think about a blockchain:

- Digital: It exists purely as computer code.

- Distributed: No single entity owns or controls it; copies are spread across a vast network of computers (nodes).

- Decentralized: There’s no central authority or server. Participants communicate directly with each other.

- Public (often): Most blockchains are open and transparent, meaning anyone can view the transactions.

- Immutable: Once a record is added, it cannot be changed or deleted.

The "chain" part comes from the way these records (called "blocks") are cryptographically linked together, forming an unbreakable sequence.

The Anatomy of a Block: What’s Inside?

Before we dive into how blocks are linked, let’s understand what a single "block" contains. Think of a block as a page in our digital record book. Each page is filled with information, primarily:

- Transaction Data: This is the core of the block. For cryptocurrencies, it would be details like "Alice sent 1 Bitcoin to Bob," including sender, receiver, amount, and a timestamp. For other applications, it could be medical records, supply chain details, or voting results.

- Timestamp: The exact date and time the block was created.

- Cryptographic Hash of the Current Block: A unique digital fingerprint of all the data within this specific block. Even a tiny change to the data inside the block would completely alter this hash.

- Cryptographic Hash of the Previous Block: This is the crucial link! It’s the digital fingerprint of the block that came directly before it in the chain. This is what creates the "chain" and makes the entire ledger incredibly secure.

- Nonce (Number Used Once): A random number used in the "mining" process (which we’ll explain shortly) to find the correct hash for the block.

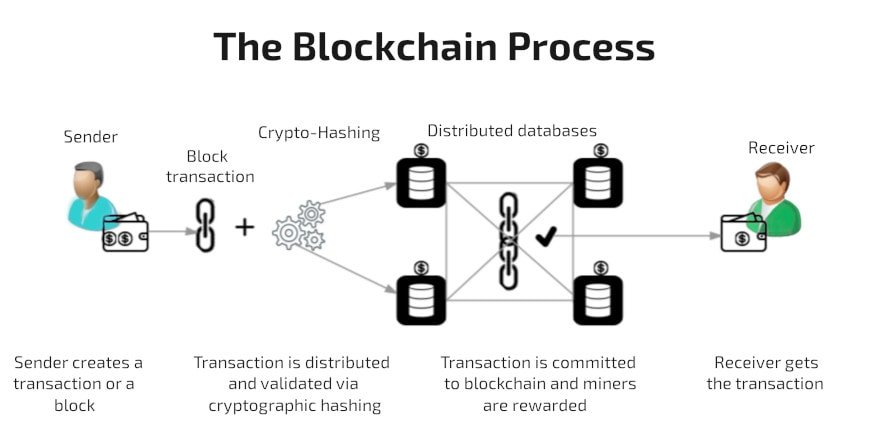

How a Transaction Becomes a Block: A Step-by-Step Journey

Let’s follow the journey of a typical transaction on a blockchain, like sending cryptocurrency from one person to another.

Step 1: A Transaction is Initiated

Let’s say Sarah wants to send 0.5 Bitcoin to Mark. She initiates this transaction using her cryptocurrency wallet. This transaction is digitally signed with her private key, proving her ownership of the funds.

Step 2: The Transaction is Broadcast to the Network

Once signed, Sarah’s transaction isn’t sent to a central bank. Instead, it’s broadcast to the entire Bitcoin network. This network is made up of thousands of individual computers around the world, known as nodes.

Step 3: Nodes Verify the Transaction

Each node on the network receives the broadcasted transaction. Before accepting it, they perform several checks:

- Is Sarah’s digital signature valid?

- Does Sarah have sufficient funds to make this transaction?

- Has this transaction already been spent (to prevent double-spending)?

If the transaction passes these checks, the nodes consider it valid and add it to a pool of unconfirmed transactions.

Step 4: Transactions are Grouped into a Block

Special nodes on the network, called miners (or validators in some blockchain types), collect a group of these valid, unconfirmed transactions. They then begin the complex process of assembling these transactions into a new block.

Step 5: Miners Solve a Complex Cryptographic Puzzle (Proof-of-Work)

This is where the "mining" aspect comes in, particularly for blockchains using a Proof-of-Work (PoW) consensus mechanism (like Bitcoin). Miners compete against each other to be the first to solve a difficult mathematical puzzle. This puzzle involves finding a specific nonce (number used once) that, when combined with the block’s data and run through a hashing algorithm, produces a hash that meets a specific target requirement (e.g., starts with a certain number of zeros).

- Analogy: Imagine trying to find a specific needle in a giant haystack, and the only way to check is to try every single piece of hay. It’s computationally intensive trial-and-error.

The first miner to find the correct nonce and generate the valid hash for the new block "wins" the right to add the block to the blockchain and receives a reward (e.g., newly minted cryptocurrency plus transaction fees).

Step 6: The New Block is Added to the Chain

Once a miner successfully finds the valid hash and creates the new block, they broadcast it to the entire network. All other nodes verify the new block’s validity (checking the hash, transactions, etc.). If it’s valid, they accept it and add it to their own copy of the blockchain.

Step 7: The Network Updates and Repeats

With the new block added, Sarah’s transaction is now permanently recorded on the blockchain. Every node updates its ledger, and the process begins again with new transactions forming the next block in the chain.

Key Pillars of Blockchain Technology

Understanding these core concepts is crucial to grasping blockchain’s power:

1. Decentralization: No Single Point of Failure

Unlike traditional systems controlled by a single entity (like a bank or a government server), blockchain operates on a peer-to-peer (P2P) network. This means:

- No Central Authority: No single company, person, or server controls the entire network.

- Distributed Copies: Every participant (node) has a full copy of the entire blockchain ledger.

- Resilience: If one node goes offline, the network continues to function seamlessly because thousands of other nodes maintain the ledger. There’s no single point of attack or failure.

2. Cryptography & Hashing: The Digital Fingerprint

Cryptography is the backbone of blockchain security. Specifically, hashing plays a vital role.

- What is a Hash? A hash function takes any input data (text, numbers, files) and converts it into a fixed-length string of characters (the "hash" or "digital fingerprint"). For example, the SHA-256 algorithm (commonly used in Bitcoin) will always produce a 256-bit (64-character) hash, no matter how small or large the input.

- Unique and Deterministic: The same input will always produce the same hash. Even a minuscule change in the input data will result in a completely different hash.

- One-Way: It’s virtually impossible to reverse-engineer the original data from its hash.

This hashing mechanism is what links blocks together: each block contains the hash of the previous block. If someone tries to tamper with an old transaction in an earlier block, its hash would change. This would then invalidate the hash stored in the next block, and so on, breaking the entire chain and immediately alerting the network to the fraudulent activity.

3. Immutability: Once Written, Forever Set

Thanks to the cryptographic linking of blocks and the distributed nature of the network, blockchain records are virtually immutable.

- Once a block of transactions is added to the chain and verified by the network, it cannot be altered or deleted.

- To change a single transaction, a malicious actor would have to re-mine that block, then re-mine every subsequent block in the chain (because each hash would change), and then somehow gain control of over 51% of the entire network’s computing power to override the legitimate chain. This is astronomically difficult and expensive, making tampering impractical for large, established blockchains.

4. Consensus Mechanisms: How Everyone Agrees

With no central authority, how does a decentralized network agree on the correct version of the ledger? This is where consensus mechanisms come in. They are algorithms that ensure all participants in the network agree on the validity of transactions and the state of the blockchain.

- Proof-of-Work (PoW): (As explained above) Miners expend significant computational effort to solve a puzzle. The first to solve it gets to add the new block. This energy expenditure makes it difficult and costly to attack the network. Bitcoin and Ethereum (until recently) use PoW.

- Proof-of-Stake (PoS): An alternative to PoW. Instead of competing with computing power, participants (validators) "stake" (lock up) a certain amount of their cryptocurrency as collateral. The more they stake, the higher their chance of being chosen to validate the next block. If they act maliciously, their staked crypto can be slashed. PoS is more energy-efficient than PoW. Ethereum has transitioned to PoS.

- There are many other consensus mechanisms (e.g., Delegated Proof-of-Stake, Proof-of-Authority), each with its own trade-offs in terms of security, scalability, and decentralization.

5. Transparency (with Pseudonymity): Open Yet Private

Most public blockchains offer a unique blend of transparency and pseudonymity:

- Transparency: All transactions on the blockchain are publicly visible. Anyone can view the entire transaction history from the genesis block (the first block) to the latest one.

- Pseudonymity: While transactions are public, the identities of the participants are not directly revealed. Instead, they are represented by alphanumeric addresses (like a bank account number without your name attached). While activity can be traced to an address, linking that address to a real-world identity often requires additional information.

Why Blockchain Matters: The Benefits of Distributed Ledgers

The unique characteristics of blockchain technology offer several compelling advantages over traditional systems:

- Increased Trust: By removing the need for intermediaries, blockchain inherently builds trust into the system. You don’t need to trust a bank; you trust the cryptographic proof and the network’s consensus.

- Enhanced Security: The immutability and decentralized nature make blockchains highly resistant to fraud and cyberattacks. Tampering with data is incredibly difficult.

- Transparency & Auditability: Every transaction is recorded and publicly verifiable, making it easy to audit and track information.

- Efficiency & Speed: Transactions can often be processed faster and at lower costs than traditional systems, especially for international transfers, as they don’t rely on multiple intermediaries.

- Reduced Costs: Eliminating intermediaries can cut down on fees and operational expenses.

- Resilience: The distributed network ensures there’s no single point of failure.

Beyond Cryptocurrency: Real-World Applications of Blockchain

While Bitcoin and other cryptocurrencies brought blockchain into the mainstream, the underlying technology has far-reaching potential across various industries:

- Supply Chain Management: Tracking products from origin to consumer, ensuring authenticity and transparency.

- Healthcare: Securely managing patient records, ensuring data integrity and privacy, and facilitating interoperability.

- Voting Systems: Creating tamper-proof and transparent election processes.

- Digital Identity: Securely managing personal identities, allowing individuals more control over their data.

- Real Estate: Streamlining property transfers, reducing fraud, and speeding up transactions.

- Intellectual Property: Proving ownership and timestamping creative works.

- Gaming & NFTs (Non-Fungible Tokens): Creating unique, verifiable digital assets and enabling true ownership of in-game items.

- Smart Contracts: Self-executing agreements where the terms are directly written into code, automatically executing when conditions are met.

Common Misconceptions About Blockchain

- Blockchain is only for Bitcoin/Cryptocurrency: While it underpins cryptocurrencies, blockchain is a foundational technology with applications far beyond digital money.

- Blockchain is completely anonymous: While addresses are pseudonymous, advanced analysis can sometimes link addresses to real-world identities, especially if transactions interact with regulated entities.

- Blockchain is infallible/unhackable: While highly secure, no system is 100% impenetrable. Vulnerabilities can arise from coding errors, poorly designed protocols, or external attacks on supporting infrastructure. However, the blockchain itself is incredibly robust.

Conclusion: The Future is Distributed

Understanding how blockchain works is no longer just for tech enthusiasts; it’s becoming essential knowledge in our increasingly digital world. From the simple concept of a shared digital ledger to the intricate dance of cryptographic hashes, consensus mechanisms, and decentralized networks, blockchain represents a fundamental shift in how we can build trust and manage information.

By offering unparalleled security, transparency, and efficiency, blockchain is poised to revolutionize industries, empower individuals, and redefine the very nature of digital interactions. As this technology continues to evolve, its impact will only grow, paving the way for a more distributed, secure, and transparent future.

Frequently Asked Questions (FAQs)

Q1: Is blockchain only used for cryptocurrencies like Bitcoin?

A1: No, while cryptocurrencies are the most well-known application, blockchain technology can be used for any system that requires a secure, immutable, and transparent record of transactions or data. This includes supply chain tracking, digital identity, healthcare records, voting systems, and more.

Q2: Is blockchain truly secure? Can it be hacked?

A2: Blockchain is highly secure due to its decentralized nature, cryptographic hashing, and immutability. To alter a record, a malicious actor would need to control a significant portion (often over 51%) of the network’s computing power and re-mine multiple blocks, which is practically impossible for large, established blockchains. While the blockchain itself is robust, vulnerabilities can exist in applications built on top of it or in user practices (e.g., losing private keys).

Q3: Who controls the blockchain?

A3: No single entity controls a decentralized blockchain. It is maintained and validated by the collective network of participants (nodes) who adhere to the protocol’s rules. This distributed control is a core principle of blockchain technology.

Q4: Can a blockchain be changed or deleted?

A4: Once a transaction or block is added to the blockchain and confirmed, it is designed to be immutable, meaning it cannot be changed or deleted. This is because each block contains a cryptographic hash of the previous block, creating an unbreakable chain. Any attempt to alter an old block would change its hash, breaking the link and immediately being detected by the network.

Q5: What is a "node" in blockchain?

A5: A node is a computer connected to the blockchain network. It runs the blockchain software, maintains a copy of the entire ledger, validates transactions, and participates in the network’s consensus process. Nodes are essential for the decentralization and security of the blockchain.

Post Comment