Unlocking the Global Marketplace: Your Beginner’s Guide to International Trade & Economics

The world is more interconnected than ever before. From the coffee you drink to the smartphone in your pocket, countless products and services cross international borders every single day. This vast web of transactions is what we call international trade, and understanding its fundamentals is key to grasping how the global economy works.

Whether you’re a student, an aspiring entrepreneur, or simply curious about the forces shaping our world, this comprehensive guide will break down the core concepts of international trade and economics into easy-to-understand ideas. Get ready to embark on a journey that reveals the fascinating dynamics of our global marketplace!

I. What is International Trade? The Basics of Global Exchange

At its heart, international trade is simply the exchange of goods, services, and capital across national borders. It’s an extension of the trade we do every day, but on a much grander, global scale.

- Definition of International Trade: The buying and selling of goods and services between different countries.

- Goods (Merchandise Trade): Tangible products like cars, clothing, food, and electronics.

- Services (Invisible Trade): Intangible products like tourism, banking, consulting, software development, and transportation.

- Capital Flows: The movement of money for investment purposes across borders (e.g., buying foreign stocks, building factories abroad).

- Globalization: The increasing interconnectedness and interdependence of countries through the flow of goods, services, capital, technology, and information.

- Why Countries Trade: Countries trade because they can’t produce everything they need or want efficiently, or because other countries can produce certain things better or cheaper.

- Interdependence: International trade fosters interdependence, meaning countries rely on each other for various goods and services.

- Domestic Trade vs. International Trade: Domestic trade occurs within a country’s borders, while international trade crosses them, introducing complexities like different currencies, laws, and cultures.

II. Why Do Nations Trade? The Core Economic Theories

Understanding why countries engage in trade is fundamental. Economists have developed several theories to explain the patterns and benefits of international exchange.

A. The Foundation: Scarcity & Specialization

- Scarcity: Resources (land, labor, capital) are limited, forcing countries to make choices about what to produce.

- Specialization: Countries focus on producing goods and services they are relatively good at, then trade for what they need.

- Efficiency: Specialization leads to greater efficiency in production.

- Increased Output: When countries specialize and trade, the total global output of goods and services increases.

B. Classical Theories: Absolute & Comparative Advantage

- Absolute Advantage (Adam Smith): A country has an absolute advantage if it can produce a good more efficiently (using fewer resources) than another country.

- Example: If Country A can produce 10 cars with 100 workers, and Country B can produce only 5 cars with 100 workers, Country A has an absolute advantage in cars.

- Comparative Advantage (David Ricardo): A country has a comparative advantage if it can produce a good at a lower opportunity cost than another country. This is the most crucial concept in international trade.

- Opportunity Cost: What you give up to get something else. In trade, it’s the amount of one good that must be sacrificed to produce more of another good.

- Example: If Country A can produce 10 cars or 20 TVs with the same resources, and Country B can produce 5 cars or 25 TVs, Country A has a comparative advantage in cars (opportunity cost of 2 TVs per car vs. Country B’s 5 TVs per car), while Country B has a comparative advantage in TVs.

- Gains from Trade: Even if one country has an absolute advantage in everything, both countries can still benefit from trade by specializing in their comparative advantage.

- Mutual Benefit: Trade based on comparative advantage ensures that all participating countries can improve their welfare.

C. Modern Theories: Explaining Diverse Trade Patterns

- Heckscher-Ohlin Theory (Factor Endowments): Countries export goods that intensively use their abundant and cheap factors of production (e.g., labor-abundant countries export labor-intensive goods).

- Factor Endowments: The quantity and quality of a country’s factors of production (land, labor, capital, technology).

- Leontief Paradox: An empirical finding that challenged the Heckscher-Ohlin theory, showing that the U.S. (capital-abundant) exported labor-intensive goods and imported capital-intensive goods. This led to further refinements in trade theory.

- New Trade Theory (Paul Krugman): Explains trade between similar countries, often in similar products, driven by economies of scale and product differentiation.

- Economies of Scale: As production increases, the cost per unit decreases, making larger producers more competitive.

- First-Mover Advantage: The economic and strategic advantages gained by being the first to enter an industry or market.

- Product Life Cycle Theory (Raymond Vernon): Products go through stages (new, maturing, standardized), and trade patterns change accordingly (e.g., product initially produced and consumed in the innovating country, then exported, then eventually produced in lower-cost countries).

- Porter’s Diamond (National Competitive Advantage): Examines why certain industries in certain nations are more competitive globally, based on factors like factor endowments, domestic demand, related industries, and firm strategy/rivalry.

III. The Benefits of International Trade: Why We Do It

The widespread engagement in international trade isn’t just about economic theory; it brings tangible benefits to consumers, businesses, and entire economies.

- Lower Prices for Consumers: Competition from imports often drives down prices for domestic goods.

- Greater Variety of Goods and Services: Consumers have access to products not produced domestically.

- Access to Resources: Countries can acquire raw materials or components they lack domestically.

- Increased Competition: Forces domestic producers to be more efficient and innovative.

- Economies of Scale: Firms can produce for a larger global market, allowing them to achieve greater efficiency and lower per-unit costs.

- Enhanced Innovation and Technology Transfer: Trade facilitates the spread of new ideas, technologies, and production methods across borders.

- Economic Growth: Trade stimulates economic activity, leading to higher GDP and income levels.

- Job Creation: Export-oriented industries can create new jobs.

- Improved Quality: Competition encourages producers to improve the quality of their products.

- Increased Choice: More options for consumers in terms of brands, styles, and features.

- Cultural Exchange and Understanding: Trade often goes hand-in-hand with increased cultural interaction.

- Better Allocation of Resources: Resources are directed to their most productive uses globally.

- Higher Standards of Living: Access to a wider range of affordable goods and services improves overall welfare.

IV. Barriers to International Trade: When Governments Intervene

Despite the many benefits, governments often impose restrictions on international trade. These restrictions are known as trade barriers or protectionism.

A. Tariffs: The Taxes on Imports

- Tariff Definition: A tax or duty imposed on imported goods or services.

- Purpose of Tariffs: To make imported goods more expensive, thereby making domestic goods more competitive.

- Revenue Tariffs: Imposed to generate government revenue.

- Protective Tariffs: Imposed to protect domestic industries from foreign competition.

- Specific Tariffs: A fixed charge per unit of imported good (e.g., $10 per ton of steel).

- Ad Valorem Tariffs: A percentage of the imported good’s value (e.g., 5% of the car’s value).

- Impact of Tariffs:

- Higher prices for consumers.

- Reduced imports.

- Increased domestic production (sometimes inefficiently).

- Potential for trade wars (retaliatory tariffs).

- Reduced overall trade volume.

B. Non-Tariff Barriers (NTBs): Beyond Taxes

- Non-Tariff Barriers (NTBs) Definition: Any non-tax measure that restricts international trade.

- Import Quotas: A physical limit on the quantity of a good that can be imported over a specific period.

- Impact: Raises prices, limits choice, benefits domestic producers.

- Voluntary Export Restraints (VERs): A quota on trade imposed by the exporting country, usually at the request of the importing country.

- Subsidies: Government payments to domestic producers, making their products cheaper and more competitive against imports.

- Impact: Can lead to overproduction, distort markets, and provoke complaints from other countries.

- Embargoes: A complete ban on trade with a particular country or on a specific good, often for political reasons.

- Administrative Barriers: Complex customs procedures, bureaucratic delays, and excessive paperwork that make importing difficult.

- Health and Safety Standards: Regulations on product quality, safety, or environmental impact that can unintentionally (or intentionally) act as trade barriers.

- Local Content Requirements: Rules specifying that a certain percentage of a product’s value must be produced domestically.

- Anti-dumping Duties: Tariffs imposed on imported goods that are priced below their production cost or domestic market price in the exporting country (dumping).

- Boycotts: A refusal to purchase goods or services from a particular country or company.

C. Arguments for Protectionism: Why Governments Use Barriers

- Infant Industry Argument: Protecting new domestic industries until they are mature enough to compete globally.

- National Security Argument: Protecting industries deemed vital for national defense (e.g., defense, energy, food).

- Job Protection Argument: Shielding domestic jobs from foreign competition.

- Dumping Argument: Counteracting "dumping" by foreign firms (selling goods below cost to gain market share).

- Environmental Protection Argument: Preventing imports from countries with lax environmental standards.

- Labor Standards Argument: Protecting domestic workers from competition with countries that have lower labor costs or poor working conditions.

- Retaliation Argument: Imposing barriers in response to another country’s unfair trade practices.

- Revenue Argument: Tariffs can be a source of government revenue, especially in developing countries.

- Strategic Trade Policy: Government intervention to help domestic firms gain advantages in global industries, often involving subsidies or R&D support.

V. Understanding Exchange Rates: The Currency Connection

International trade relies on converting one currency into another. This is where exchange rates come in.

- Exchange Rate Definition: The price of one currency in terms of another currency.

- Direct Quote: How much foreign currency you get for one unit of your domestic currency (e.g., $1 USD = 0.90 Euro).

- Indirect Quote: How much domestic currency you need to buy one unit of foreign currency (e.g., 1 Euro = $1.11 USD).

- Appreciation: When a currency becomes stronger, meaning it can buy more of a foreign currency.

- Impact: Makes exports more expensive and imports cheaper.

- Depreciation: When a currency becomes weaker, meaning it can buy less of a foreign currency.

- Impact: Makes exports cheaper and imports more expensive.

- Factors Influencing Exchange Rates:

- Interest Rates: Higher interest rates often attract foreign investment, increasing demand for the currency.

- Inflation: Higher inflation tends to weaken a currency’s purchasing power.

- Economic Performance: Strong economic growth can attract investment and strengthen a currency.

- Political Stability: Stable political environments are more attractive to investors.

- Speculation: Traders buying or selling currencies based on anticipated future movements.

- Balance of Payments: Surpluses or deficits can influence currency demand.

- Fixed Exchange Rate System: A government or central bank ties its currency’s value to another currency or a basket of currencies, or to a commodity like gold.

- Floating Exchange Rate System: The value of a currency is determined by supply and demand in the foreign exchange market. Most major currencies today are floating.

- Managed Float: A system where the exchange rate is mostly determined by market forces, but the central bank may intervene occasionally to smooth out excessive fluctuations.

- Impact on Exports: A weaker domestic currency makes exports more competitive.

- Impact on Imports: A stronger domestic currency makes imports cheaper.

VI. The Balance of Payments: A Nation’s Financial Scorecard

The Balance of Payments (BoP) is a summary of all economic transactions between a country and the rest of the world over a specific period (usually a year). It’s always in balance, though its sub-accounts may show surpluses or deficits.

- Balance of Payments (BoP) Definition: A systematic record of all economic transactions between residents of one country and residents of all other countries.

- Current Account: Records trade in goods and services, investment income, and current transfers.

- Trade Balance: Exports of goods minus imports of goods.

- Services Balance: Exports of services minus imports of services.

- Income Balance: Net income from investments abroad (e.g., dividends, interest).

- Current Transfers: One-way transfers like foreign aid, remittances, or gifts.

- Capital Account (or Financial Account): Records international capital transfers and transactions in financial assets.

- Foreign Direct Investment (FDI): Investment in physical assets or control of foreign companies (e.g., building a factory abroad).

- Portfolio Investment: Investment in financial assets like stocks and bonds, without gaining control.

- Current Account Deficit: When a country imports more goods and services, pays out more income, and makes more transfers than it receives. It implies borrowing from abroad or selling off assets.

- Current Account Surplus: When a country exports more goods and services, receives more income, and gets more transfers than it pays out. It implies lending to abroad or accumulating foreign assets.

- Relationship between Current and Capital Accounts: A current account deficit must be financed by a capital account surplus (more money flowing into the country for investment than flowing out), and vice versa.

- Implications of Deficits/Surpluses:

- Persistent deficits can indicate reliance on foreign borrowing or a decline in competitiveness.

- Persistent surpluses can indicate strong competitiveness or insufficient domestic investment opportunities.

VII. Global Economic Organizations & Agreements: Shaping the Rules

To manage the complexities of international trade and finance, various global organizations and agreements have been established.

- World Trade Organization (WTO): The primary international organization dealing with the rules of trade between nations.

- History (GATT): Evolved from the General Agreement on Tariffs and Trade (GATT) established in 1948.

- Purpose: To help trade flow as smoothly, predictably, and freely as possible.

- Functions: Administering trade agreements, acting as a forum for trade negotiations, handling trade disputes, monitoring national trade policies.

- International Monetary Fund (IMF): Works to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty.

- World Bank Group: Provides financial and technical assistance to developing countries around the world. Its mission is to reduce poverty and support development.

- Regional Economic Integration: Agreements among countries in a geographic region to reduce and ultimately remove tariff and non-tariff barriers to the free flow of goods, services, and factors of production.

- Free Trade Area (FTA): Members eliminate all barriers to trade among themselves but retain independent trade policies with non-member countries (e.g., NAFTA/USMCA).

- Customs Union: Members eliminate internal trade barriers and adopt a common external trade policy against non-member countries (e.g., MERCOSUR).

- Common Market: Members form a customs union and allow for the free movement of factors of production (labor and capital) among themselves (e.g., European Economic Community before becoming the EU).

- Economic Union: Members form a common market and coordinate economic policies (e.g., common currency, common fiscal policy) (e.g., European Union).

- Political Union: Members integrate economic and political policies, potentially leading to a single government.

- European Union (EU): A prominent example of an economic and political union, with a common market, common currency (Eurozone), and harmonized regulations.

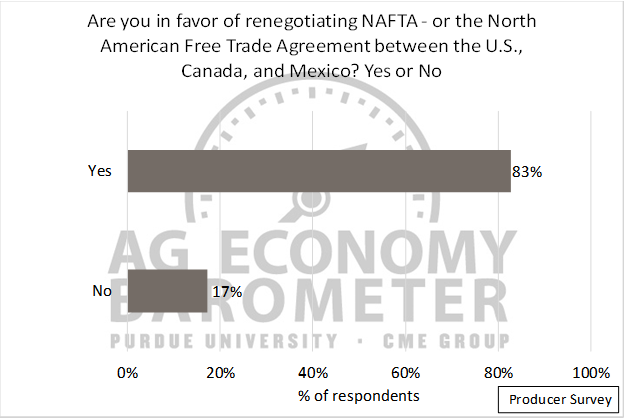

- North American Free Trade Agreement (NAFTA) / USMCA: A free trade agreement between the United States, Mexico, and Canada.

- Association of Southeast Asian Nations (ASEAN): A political and economic union of 10 member states in Southeast Asia.

- MERCOSUR: A South American trade bloc.

- APEC (Asia-Pacific Economic Cooperation): A forum of 21 Pacific Rim member economies that promotes free trade throughout the Asia-Pacific region.

VIII. Key Economic Concepts in a Global Context

To fully appreciate international trade, it’s helpful to understand some broader economic concepts as they apply globally.

- Gross Domestic Product (GDP): The total monetary value of all final goods and services produced within a country’s borders in a specific time period. Trade is a significant component.

- Inflation: The rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. Global trade can influence inflation.

- Deflation: The opposite of inflation; a decrease in the general price level of goods and services.

- Recession: A significant decline in economic activity spread across the economy, generally identified by two consecutive quarters of negative GDP growth. Global trade can exacerbate or mitigate recessions.

- Economic Sanctions: Penalties applied by one country or a group of countries on another, often for political reasons, restricting trade and financial transactions.

- Supply Chain: The entire process of producing and distributing a product, from raw materials to the final consumer. Global supply chains are complex and span multiple countries.

- Protectionism vs. Free Trade: The ongoing debate about whether governments should restrict trade (protectionism) or allow it to flow freely (free trade).

- Doha Round: A round of WTO trade negotiations that began in 2001, aiming to lower trade barriers around the world, but largely stalled due to disagreements.

- Trade Deficit/Surplus: When a country imports more than it exports (deficit) or exports more than it imports (surplus) over a given period.

Conclusion: Your Gateway to Global Understanding

You’ve now taken your first major step into understanding the fundamentals of international trade and economics. From the basic principles of why countries trade to the complex web of global organizations and financial flows, you’ve gained insight into the forces that shape our interconnected world.

This knowledge is not just for economists; it empowers you to better understand news headlines, make informed consumer choices, and even consider future career paths in a globalized economy. The world of trade is dynamic, constantly evolving with new technologies, political shifts, and environmental challenges. But with these foundational concepts, you’re well-equipped to continue your journey of learning and discovery in the fascinating global marketplace!

Post Comment