Mastering Your Money: How to Build a Cash Flow Projection Model (Beginner’s Guide)

Introduction: Why Your Business (or Life!) Needs a Cash Flow Projection

Imagine your business is a ship sailing the open seas. You’ve got a crew, cargo, and a destination. But what if you run out of fuel mid-ocean? Or hit an iceberg you didn’t see coming? That’s what happens to businesses (and personal finances) without a clear understanding of their cash flow.

Many people confuse "profit" with "cash." You can be profitable on paper but still run out of cash – a phenomenon often called "profitless growth." This is why understanding your cash flow is not just important; it’s absolutely critical for survival and growth.

A Cash Flow Projection Model is like your ship’s radar and fuel gauge combined. It’s a forward-looking estimate of how much cash you expect to come into your business and how much you expect to go out over a specific period. It helps you anticipate shortages, plan for growth, make informed decisions, and ultimately, stay afloat and thrive.

Whether you’re a budding entrepreneur, a small business owner, or simply want to get a better handle on your personal finances, this comprehensive guide will walk you through building your own cash flow projection model, step-by-step, in a way that’s easy to understand.

What is a Cash Flow Projection Model and Why Do You Need One?

Let’s break down the core concept before we dive into building one.

What is it?

A Cash Flow Projection Model (also known as a cash flow forecast) is a financial tool that estimates the cash you expect to receive (inflows) and the cash you expect to pay out (outflows) over a future period. It’s usually done for weekly, monthly, quarterly, or annual periods.

Think of it as looking at your checking account balance, but for the future. You’re predicting what your balance will be after all the money comes in and all the bills go out.

Why is it Crucial?

- Avoid Cash Shortfalls: The most important reason! It helps you see potential cash shortages before they happen, giving you time to find solutions (e.g., secure a line of credit, delay non-essential payments, accelerate receivables).

- Strategic Decision-Making:

- Expansion: Do you have enough cash to hire new staff, open a new location, or invest in new equipment?

- Inventory: Can you afford to buy more inventory to meet demand?

- Debt Repayment: Can you comfortably service your debts?

- Pricing: Does your pricing generate enough cash to cover costs?

- Secure Funding: Lenders and investors will almost always ask for a detailed cash flow projection. It shows them you understand your business’s financial health and have a plan.

- Measure Performance: By comparing your actual cash flow to your projections, you can identify trends, understand what’s working (or not), and refine your future forecasts.

- Identify Opportunities: Spot periods of surplus cash that you could invest, save, or use for strategic initiatives.

Cash Flow vs. Profit: A Critical Distinction for Beginners

This is where many beginners get confused.

- Profit (from your Income Statement/P&L) is about whether your revenues exceed your expenses during a period. It includes non-cash items like depreciation and doesn’t account for when cash actually changes hands. For example, you might make a big sale on credit, booking the revenue now, but the cash won’t arrive for 30-60 days.

- Cash Flow (from your Cash Flow Statement or Projection) is about the actual movement of money in and out of your bank account. It focuses solely on cash receipts and cash payments.

You can be profitable but cash-poor (e.g., lots of sales on credit, high inventory, slow collections). Conversely, you can have strong cash flow even if your profits are low (e.g., selling off assets, taking out a loan). Cash is king because you pay bills with cash, not profit.

The Essential Components of Your Cash Flow Model

Every cash flow projection model, whether simple or complex, revolves around a few key elements:

- Starting Cash Balance: The amount of cash you have in your bank account(s) at the very beginning of the projection period. This is your foundation.

- Cash Inflows (Sources of Cash): All the money you expect to receive. This is not just sales!

- Sales revenue (from customers paying cash or previously extended credit)

- Loan proceeds

- Investment capital

- Sale of assets

- Interest income

- Grants or subsidies

- Cash Outflows (Uses of Cash): All the money you expect to pay out.

- Operating expenses (rent, utilities, salaries, marketing, insurance, supplies)

- Cost of Goods Sold (COGS) / Cost of Sales (purchases of raw materials or finished goods)

- Loan repayments (principal and interest)

- Capital expenditures (buying equipment, vehicles, property)

- Taxes

- Owner’s draws or dividends

- Net Cash Flow: This is simply your total cash inflows minus your total cash outflows for a given period.

- If positive, you had more cash come in than go out.

- If negative, you spent more cash than you received.

-

Ending Cash Balance: Your starting cash balance plus your net cash flow for the period. This ending balance then becomes the starting balance for the next period.

Formula:

Ending Cash Balance = Starting Cash Balance + Total Cash Inflows - Total Cash Outflows

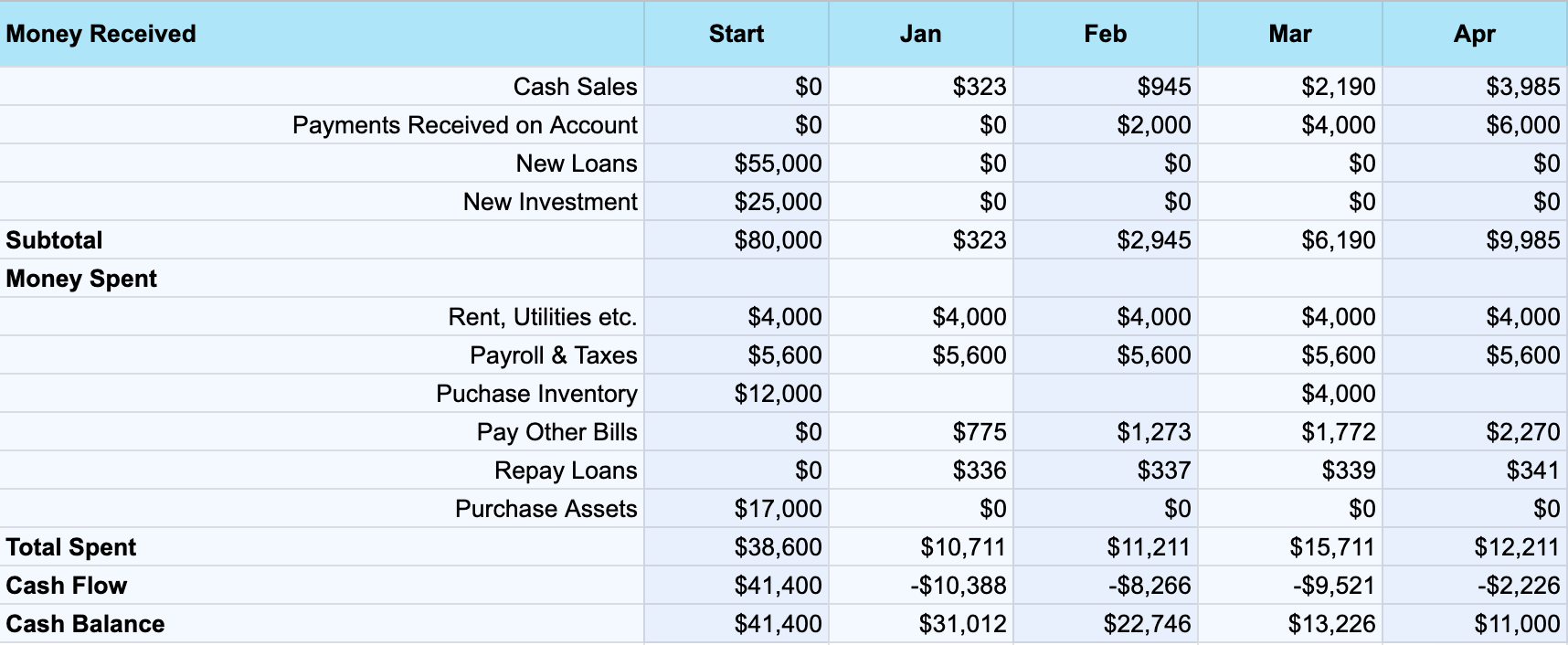

Step-by-Step Guide: How to Build Your Cash Flow Projection Model

Now, let’s roll up our sleeves and build your model. We’ll assume you’re using a spreadsheet program like Microsoft Excel or Google Sheets, as they are the most accessible and flexible tools for beginners.

Step 1: Choose Your Timeframe

Before you start, decide how far into the future you want to project and in what increments.

- Short-term (1-3 months, weekly or bi-weekly increments): Excellent for managing immediate liquidity, payroll, and supplier payments. Ideal for new businesses or those with volatile cash flows.

- Medium-term (3-12 months, monthly increments): Good for operational planning, identifying seasonal trends, and planning for larger expenditures.

- Long-term (1-3 years, quarterly or annual increments): Useful for strategic planning, securing long-term financing, and forecasting major investments.

Recommendation for beginners: Start with a monthly projection for the next 6-12 months. This offers a good balance of detail and manageability.

Step 2: Gather Your Data

You’ll need information from your past and your best guesses for the future.

- Historical Data:

- Bank statements (actual cash balances, past inflows/outflows).

- Income Statements (Profit & Loss statements).

- Balance Sheets.

- Past invoices (sales and purchases).

- Payroll records.

- Future Estimates:

- Sales forecasts (how much do you expect to sell, and when will you get paid?).

- Planned expenses (rent, loan payments, subscriptions, salaries).

- Anticipated one-time expenses (equipment purchase, major marketing campaign).

- Planned financing (new loans, investments).

Step 3: Determine Your Starting Cash Balance

This is straightforward. Look at your bank account balance(s) as of the first day of your projection period. This is the cash you have on hand right now.

- Example: If you’re starting a monthly projection for January, what was your total cash in the bank on January 1st? Let’s say it’s $10,000.

Step 4: Project Your Cash Inflows

This is where you estimate all the money coming into your business. Be as realistic as possible – it’s better to underestimate slightly than to wildly overestimate.

- Sales Revenue:

- Cash Sales: If customers pay immediately, that’s easy.

- Credit Sales: If you offer payment terms (e.g., Net 30 days), only project the cash inflow for when you expect to receive the money, not when you make the sale. For example, if you make $5,000 in credit sales in January with Net 30 terms, that cash inflow will appear in February.

- How to estimate: Use historical sales data, market trends, confirmed orders, and your marketing/sales pipeline.

- Loan Proceeds: If you anticipate taking out a loan, project the amount and when you expect to receive the funds.

- Investment Capital: If investors are putting money into your business, when will that cash hit your account?

- Other Income: Any other expected cash receipts (e.g., refunds, interest earned, grants).

Spreadsheet Tip: Create a dedicated section for "Cash Inflows." List each type of inflow as a row and the months/periods as columns.

| Cash Inflows | Jan | Feb | Mar | Apr |

|---|---|---|---|---|

| Cash Sales | $3,000 | $3,200 | $3,500 | $3,700 |

| Collections from Credit Sales (Prior Month) | $2,000 | $2,500 | $2,800 | $3,000 |

| Loan Proceeds | $0 | $10,000 | $0 | $0 |

| Total Cash Inflows | $5,000 | $15,700 | $6,300 | $6,700 |

Step 5: Project Your Cash Outflows

This is where you list all the money you expect to spend. Be thorough and account for every expense. Categorize them to make it easier to track.

- Cost of Goods Sold (COGS) / Direct Costs: The costs directly associated with producing your goods or services.

- Inventory Purchases: When do you pay for the inventory, not when you sell it? If you buy on credit, project the payment when it’s due.

- Labor (Direct): Wages paid to those directly involved in production.

- Operating Expenses: Your regular, ongoing costs of doing business.

- Rent/Mortgage: Fixed monthly payment.

- Salaries & Wages (Indirect/Admin): Payroll, including taxes and benefits.

- Utilities: Electricity, water, internet.

- Marketing & Advertising: Ad spend, website maintenance.

- Software Subscriptions: CRM, accounting software, etc.

- Insurance: Monthly/annual premiums.

- Professional Fees: Accountant, lawyer.

- Supplies: Office supplies, cleaning supplies.

- Debt Repayments: Principal and interest payments on loans.

- Capital Expenditures (CapEx): Large purchases of assets that will be used for more than one year (e.g., new equipment, vehicles, property improvements).

- Taxes: Estimated income tax, sales tax, payroll taxes.

- Owner’s Draw/Dividends: Any money you plan to take out of the business for personal use.

Spreadsheet Tip: Create another dedicated section for "Cash Outflows." List each type of outflow as a row and the months/periods as columns.

| Cash Outflows | Jan | Feb | Mar | Apr |

|---|---|---|---|---|

| Inventory Purchases | $1,500 | $1,800 | $2,000 | $2,200 |

| Rent | $1,000 | $1,000 | $1,000 | $1,000 |

| Salaries & Wages | $1,200 | $1,200 | $1,200 | $1,200 |

| Utilities | $150 | $170 | $160 | $180 |

| Marketing | $300 | $300 | $300 | $300 |

| Loan Payment | $0 | $500 | $500 | $500 |

| Total Cash Outflows | $4,150 | $4,970 | $5,160 | $5,380 |

Step 6: Calculate Your Net Cash Flow

For each period (month), subtract your Total Cash Outflows from your Total Cash Inflows.

Formula: Net Cash Flow = Total Cash Inflows - Total Cash Outflows

| Jan | Feb | Mar | Apr | |

|---|---|---|---|---|

| Total Cash Inflows | $5,000 | $15,700 | $6,300 | $6,700 |

| Total Cash Outflows | $4,150 | $4,970 | $5,160 | $5,380 |

| Net Cash Flow | $850 | $10,730 | $1,140 | $1,320 |

Step 7: Calculate Your Ending Cash Balance

This is the crucial step that shows your projected bank balance at the end of each period.

- For the first period (January):

Ending Cash Balance (Jan) = Starting Cash Balance (Jan) + Net Cash Flow (Jan)

$10,850 = $10,000 + $850 - For subsequent periods: The ending cash balance of the previous period becomes the starting cash balance of the current period.

Ending Cash Balance (Feb) = Starting Cash Balance (Feb) + Net Cash Flow (Feb)

$21,580 = $10,850 + $10,730

| Jan | Feb | Mar | Apr | |

|---|---|---|---|---|

| Starting Cash Balance | $10,000 | $10,850 | $21,580 | $22,720 |

| Net Cash Flow | $850 | $10,730 | $1,140 | $1,320 |

| Ending Cash Balance | $10,850 | $21,580 | $22,720 | $24,040 |

Step 8: Review, Analyze, and Adjust

Once you’ve built your basic model, the real work begins.

- Look for Negative Balances: Are there any months where your ending cash balance dips below zero, or dangerously close to it? This is your early warning system!

- What to do:

- Can you delay an outflow (e.g., push back a non-essential purchase)?

- Can you accelerate an inflow (e.g., offer a discount for early payment from customers)?

- Do you need a line of credit or a short-term loan?

- Can you reduce discretionary spending?

- What to do:

- Identify Surplus Cash: Are there periods with a significant cash surplus?

- What to do:

- Can you invest this cash to earn interest?

- Is it enough to fund a planned expansion or capital expenditure?

- Can you pay down debt faster?

- What to do:

- Scenario Planning: What if sales are 20% lower than expected? What if a major expense comes up unexpectedly? Create "best-case," "worst-case," and "most likely" scenarios to understand your financial resilience.

- Set a Minimum Cash Threshold: Decide what your absolute minimum cash balance needs to be to operate comfortably (e.g., enough to cover one month’s essential expenses). If your projection falls below this, it’s a red flag.

Tools to Help You Build Your Model

While the principles remain the same, different tools can simplify the process.

-

Spreadsheets (Microsoft Excel, Google Sheets, Apple Numbers):

- Pros: Highly flexible, customizable, free (Google Sheets), powerful formulas.

- Cons: Requires manual setup, prone to human error if formulas aren’t carefully checked.

- Best for: Beginners, small businesses, anyone who wants full control and a deep understanding of the model’s mechanics.

- Pro Tip: Search online for "free cash flow projection template Excel" to get a head start.

-

Accounting Software (QuickBooks, Xero, FreshBooks):

- Pros: Automates much of the data entry, can generate reports that feed into your projection, often has built-in forecasting features.

- Cons: Can be expensive, less flexible for highly customized scenarios, sometimes focused more on historical reporting than future forecasting.

- Best for: Businesses already using these for their day-to-day accounting.

-

Dedicated Financial Planning Software:

- Pros: Designed specifically for forecasting, scenario analysis, and detailed financial modeling.

- Cons: Can be complex and expensive, often overkill for simple needs.

- Best for: Larger businesses, complex financial structures, or those needing advanced analytical capabilities.

Tips for an Effective Cash Flow Projection Model

To make your cash flow model truly useful, keep these tips in mind:

- Be Realistic (Not Optimistic!): It’s easy to inflate sales and downplay expenses. Err on the side of caution. A conservative projection is far more valuable than an overly optimistic one.

- Be Detailed, But Don’t Get Bogged Down: You don’t need to track every single paperclip. Focus on the major inflows and outflows. For smaller, recurring items, you can group them (e.g., "Office Supplies").

- Update Regularly: Your projection is a living document. Market conditions change, sales forecasts evolve, and unexpected expenses arise. Review and update your model at least monthly, or even weekly if your cash flow is volatile.

- Track Actuals Against Projections: This is how you learn and improve your forecasting accuracy. At the end of each period, compare what actually happened to what you projected. Where were you off, and why?

- Understand Your Payment Terms: For both your sales (Accounts Receivable) and your purchases (Accounts Payable), know when the cash is actually expected to move. This is key to cash flow, not just invoicing.

- Factor in Seasonality: Does your business have peak and slow seasons? Your cash flow projection must reflect these fluctuations.

- Include a "Buffer" or "Minimum Cash Balance": Always aim to have a safety net. This is cash you don’t plan to spend, reserved for emergencies or unexpected opportunities.

- Don’t Confuse Cash with Profit (Again!): Seriously, this is the biggest pitfall for beginners. Keep reminding yourself that this model is only about cash in and cash out.

- Seek Expert Help When Needed: If your business grows complex or you’re struggling, consider consulting an accountant or financial advisor. They can provide valuable insights and help you build a more robust model.

Conclusion: Take Control of Your Financial Future

Building a cash flow projection model might seem daunting at first, but it’s one of the most empowering steps you can take for your financial well-being, whether for a business or personal use. It transforms you from reacting to financial surprises to proactively planning for your future.

By diligently tracking your inflows and outflows, anticipating challenges, and identifying opportunities, you gain clarity, confidence, and control over your financial destiny. Start small, be consistent, and watch as your understanding of money grows, leading to smarter decisions and greater financial stability.

So, open that spreadsheet, gather your data, and begin building your financial radar today. Your future self (and your bank account) will thank you!

Frequently Asked Questions (FAQs) About Cash Flow Projection Models

Q1: How often should I update my cash flow projection?

A1: For most small businesses, a monthly review and update is ideal. If your cash flow is highly volatile or you’re a new business, weekly or bi-weekly might be more appropriate. For long-term strategic planning, quarterly or annual updates are sufficient.

Q2: What’s the difference between a cash flow projection and a budget?

A2: A budget is typically a plan for spending and saving over a period, often focusing on profitability or specific expense categories. A cash flow projection specifically tracks the timing of cash moving in and out, regardless of whether it’s an expense or an asset purchase. You can be within budget but still run out of cash if inflows are delayed or outflows are accelerated.

Q3: Is it okay to have a negative cash flow sometimes?

A3: Yes, temporarily. Businesses often have periods of negative cash flow, especially during growth phases (e.g., investing heavily in inventory or equipment before sales materialize) or seasonal downturns. The key is to anticipate these periods with your projection and have a plan to cover the deficit (e.g., a line of credit, savings). Persistent negative cash flow without a clear strategy is a major red flag.

Q4: How far into the future should my projection go?

A4: It depends on your purpose.

- 3-6 months: Excellent for short-term operational management and liquidity.

- 12 months: Standard for annual planning and most loan applications.

- 3-5 years: Useful for strategic planning, major investment decisions, or seeking long-term financing.

Focus on accuracy for the short-term, and understand that long-term projections will be less precise but still valuable for directional guidance.

Q5: What if my actual cash flow is very different from my projection?

A5: Don’t panic! This is a learning opportunity.

- Analyze the Variance: Identify exactly where the differences occurred (e.g., sales were lower, rent was higher, a new expense appeared).

- Understand the Cause: Was it an external factor (economic downturn, competitor action)? An internal factor (poor sales execution, unexpected equipment breakdown)? A flaw in your initial assumptions?

- Adjust Your Model: Use these insights to refine your assumptions and improve the accuracy of future projections. This iterative process is how your forecasting skills improve over time.

")

Post Comment