What is Blockchain Technology? A Simple Explanation for Beginners

In a world buzzing with talk of cryptocurrencies, NFTs, and Web3, one term stands out as the fundamental backbone: Blockchain Technology. It might sound complex, like something only tech gurus can understand, but at its heart, blockchain is a surprisingly simple yet revolutionary concept.

This article will demystify blockchain, explaining it in plain language, complete with analogies, subheadings, and bullet points to make sure you grasp the basics without getting lost in technical jargon.

Understanding the Core Concept: Imagine a Shared, Untamperable Digital Ledger

Let’s start with an analogy. Imagine you and a group of friends decide to keep a shared record of all your expenses during a trip. Instead of one person holding the master spreadsheet, you decide on a new system:

- Everyone gets a copy of the spreadsheet.

- When someone spends money, they announce it to the group.

- Everyone writes down the transaction on their copy.

- Once a set of transactions is written down, you all agree to "seal" that page (or block) and add it to your personal notebooks.

- Once a page is sealed and added, it can never be changed or removed. If someone tries to change their copy, it won’t match everyone else’s, and the group will know.

This is, in essence, what blockchain technology does on a massive, digital scale. It’s a type of Distributed Ledger Technology (DLT) where information is stored across a network of computers, rather than on a single central server.

Deconstructing the Name: "Block" + "Chain"

The name "blockchain" literally describes its structure:

The "Block"

Think of a "block" as a digital container or a page in our shared ledger. Each block is designed to hold a certain amount of information or data. What kind of data?

- Transaction Data: This is the most common type of data. For cryptocurrencies like Bitcoin, a block contains details of many transactions (e.g., "Alice sent 1 BTC to Bob," "Charlie sent 0.5 BTC to David").

- Timestamp: When the block was created.

- A Unique Code (Hash): Every block has a unique digital fingerprint, called a "hash." It’s like a unique ID for that specific block.

- The Hash of the Previous Block: This is the crucial element that creates the "chain."

The "Chain"

The "chain" refers to the way these blocks are linked together. Each new block contains the unique hash (digital fingerprint) of the block that came before it.

- This creates a chronological, unbroken chain of blocks.

- If anyone tries to alter a single transaction in an old block, that block’s hash would change.

- Since the next block in the chain contains the old hash, the chain would break, instantly revealing the tampering. This makes blockchain incredibly secure and resistant to fraud.

The Pillars of Blockchain Technology

Beyond the blocks and chains, several core principles define how blockchain works:

-

Decentralization:

- No Single Authority: Unlike traditional systems (banks, governments) that have a central controller, a blockchain network has no central server or administrator.

- Distributed Copies: Every participant (called a "node") in the network has a full copy of the entire blockchain ledger.

- Why it Matters: This eliminates a single point of failure and makes the system much harder to attack or censor. If one computer goes offline, the others keep running.

-

Immutability:

- Unchangeable Record: Once a transaction or data is recorded on the blockchain and a block is added to the chain, it cannot be altered or deleted. It’s like writing in digital stone.

- Why it Matters: This creates a permanent, auditable, and trustworthy record of all events.

-

Transparency (Pseudonymous):

- Publicly Verifiable: While your real-world identity isn’t typically linked to your blockchain address (hence "pseudonymous"), all transactions on a public blockchain are visible to everyone on the network.

- Why it Matters: This fosters trust because anyone can verify the integrity of the ledger and see the flow of assets without revealing personal details.

-

Security (Cryptography & Consensus):

- Cryptographic Hashing: As mentioned, each block is cryptographically linked to the previous one, making tampering virtually impossible.

- Consensus Mechanisms: For a new block to be added to the chain, the majority of the network’s participants must agree that the transactions within it are valid. This agreement process is called a "consensus mechanism" (e.g., Proof of Work in Bitcoin, Proof of Stake in Ethereum 2.0).

- Why it Matters: These mechanisms ensure the integrity and security of the entire network, preventing fraudulent activities.

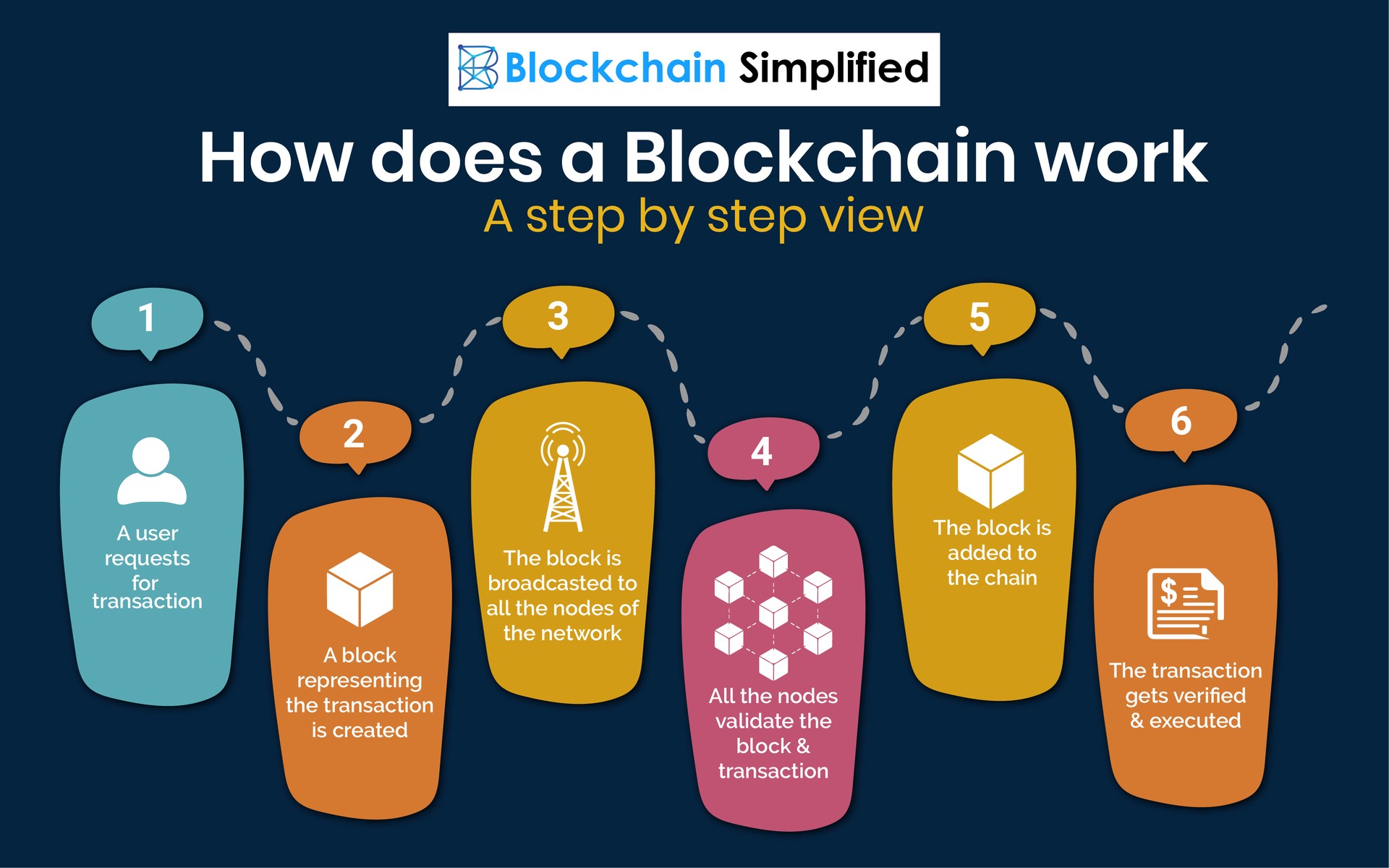

How Does a Transaction Happen on a Blockchain? (Simplified)

Let’s say Alice wants to send some cryptocurrency to Bob:

- Initiation: Alice creates a transaction (e.g., "Send 1 BTC to Bob") and digitally signs it with her private key.

- Broadcast: The transaction is broadcast to the entire blockchain network.

- Validation: "Nodes" (computers running the blockchain software) on the network receive the transaction. They verify its authenticity (Alice has enough funds, her signature is valid, etc.).

- Block Creation (Mining/Validation): Once enough valid transactions are collected, a special type of node (a "miner" or "validator," depending on the consensus mechanism) groups them into a new block. This node then works to solve a complex computational puzzle (in Proof of Work) or is chosen based on its "stake" (in Proof of Stake) to add the block to the chain.

- Chain Addition: Once the block is validated by the network (through the consensus mechanism), it is added to the existing blockchain.

- Confirmation: The transaction is now permanently recorded and irreversible. Bob receives the cryptocurrency.

Beyond Cryptocurrency: What Else Can Blockchain Do?

While cryptocurrencies like Bitcoin and Ethereum are the most famous applications, blockchain technology has potential far beyond digital money. Its ability to create secure, transparent, and immutable records makes it suitable for countless industries:

- Supply Chain Management: Tracking products from origin to consumer, ensuring authenticity and ethical sourcing. Imagine scanning a QR code on your coffee to see exactly where the beans were grown, processed, and shipped.

- Healthcare: Securely managing patient records, ensuring data privacy while allowing authorized access for doctors and researchers.

- Voting Systems: Creating transparent, tamper-proof voting systems that could increase trust in elections.

- Digital Identity: Allowing individuals to control their own digital identities, proving who they are without oversharing personal data.

- Real Estate: Streamlining property transfers, reducing fraud, and speeding up legal processes.

- Smart Contracts: Self-executing contracts where the terms of the agreement are directly written into code. Once conditions are met (e.g., payment received), the contract automatically executes its next step (e.g., releasing funds).

- Non-Fungible Tokens (NFTs): Unique digital assets (art, music, collectibles) whose ownership is verified and recorded on a blockchain.

Benefits of Blockchain Technology

The unique characteristics of blockchain bring a host of advantages:

- Increased Trust: No need to trust a central authority; trust is inherent in the network’s design.

- Enhanced Security: Highly resistant to fraud and unauthorized changes due to cryptography and decentralization.

- Greater Efficiency: Can streamline processes by removing intermediaries and automating tasks (e.g., smart contracts).

- Reduced Costs: Potentially lower transaction fees and operational costs by eliminating third parties.

- Transparency & Auditability: All participants can view the ledger, making it easy to track and verify information.

- Resilience: No single point of failure means the network is more robust and less prone to downtime.

Challenges and Limitations

Despite its potential, blockchain technology also faces hurdles:

- Scalability: Some blockchains (like Bitcoin) can process a limited number of transactions per second, leading to slower speeds and higher costs during peak times.

- Energy Consumption: Proof of Work blockchains (like Bitcoin) consume significant amounts of energy due to the computational power required for mining.

- Regulatory Uncertainty: Governments worldwide are still grappling with how to regulate blockchain and cryptocurrencies.

- Complexity: Developing and implementing blockchain solutions can be complex and requires specialized expertise.

- Adoption: Widespread adoption requires overcoming technical hurdles, educating the public, and integrating with existing systems.

Conclusion: A Foundation for the Future

Blockchain technology is more than just the engine behind Bitcoin; it’s a foundational innovation with the potential to revolutionize how we interact, transact, and trust each other in the digital world. By providing a secure, transparent, and immutable way to record information, it opens doors to new possibilities across countless industries.

While it’s still evolving and faces challenges, understanding the basics of blockchain is no longer optional. It’s a key step to comprehending the future of digital innovation and the decentralized web. As the technology matures, expect to see its impact woven into more and more aspects of our daily lives, building a more connected, efficient, and trustworthy digital future.

.png "What is Blockchain Technology? A Simple Explanation for Beginners")

Post Comment