401(k) Plans Explained: Your Ultimate Guide to Maximizing Employer Match and Securing Your Retirement

Retirement might feel like a distant dream, but the truth is, the earlier you start planning for it, the more comfortable your future self will be. One of the most powerful tools available to many employees for building a secure retirement is the 401(k) plan. And within the world of 401(k)s, there’s a "secret sauce" that can supercharge your savings: the employer match.

If you’ve ever felt overwhelmed by financial jargon or unsure how to make the most of your workplace benefits, you’re in the right place. This comprehensive guide will break down 401(k) plans in simple terms, demystify the employer match, and show you exactly how to leverage this incredible benefit to build a robust financial future.

What Exactly is a 401(k) Plan? Your Retirement Savings Superpower

Imagine a special savings account that your employer helps you set up specifically for your retirement. That’s essentially what a 401(k) plan is! It’s an employer-sponsored retirement savings and investment plan that offers significant tax advantages.

Here’s how it generally works:

- You Contribute: A portion of your paycheck is automatically deducted and deposited into your 401(k) account. You decide how much to contribute (up to annual limits set by the IRS).

- Your Employer Might Contribute: This is where the magic of the employer match comes in (more on this soon!). Many employers contribute additional money to your account based on how much you contribute.

- Your Money Grows (Tax-Advantaged): The money you and your employer contribute, along with any earnings from your investments, grow over time without being taxed each year. This "tax-deferred" growth is a huge advantage.

- You Invest: Within your 401(k), you choose from a selection of investment options, typically mutual funds, index funds, or target-date funds, which hold a variety of stocks, bonds, and other assets. This allows your money to work harder for you.

- You Withdraw in Retirement: When you reach retirement age (typically 59 ½), you can start withdrawing money from your 401(k). Depending on the type of 401(k) you have, these withdrawals will be taxed or tax-free.

Why is it called a 401(k)? It’s simply the section of the Internal Revenue Code that defines this type of plan. Nothing mysterious, just a tax code number!

Traditional 401(k) vs. Roth 401(k): Choosing Your Tax Advantage

Not all 401(k)s are created equal, especially when it comes to taxes. You’ll typically encounter two main types: the Traditional 401(k) and the Roth 401(k). Understanding the difference is key to picking the one that’s right for you.

Traditional 401(k): Tax Break Now

- Contributions: Made with "pre-tax" dollars. This means the money you contribute is deducted from your paycheck before taxes are calculated, which lowers your taxable income for the current year.

- Tax-Deferred Growth: Your investments grow over time, and you don’t pay taxes on the gains year after year.

- Withdrawals in Retirement: When you take money out in retirement, your withdrawals (both your contributions and earnings) are taxed as ordinary income.

Who it’s good for: If you believe you’re in a higher tax bracket now than you will be in retirement, or if you want to lower your current taxable income.

Roth 401(k): Tax Break Later

- Contributions: Made with "after-tax" dollars. This means taxes are already taken out of your paycheck before your contribution is made. Your taxable income for the current year isn’t reduced by these contributions.

- Tax-Free Growth: Your investments grow over time, and you don’t pay taxes on the gains.

- Tax-Free Withdrawals in Retirement: When you take money out in retirement (as long as you meet certain conditions, like being at least 59 ½ and having had the account for 5 years), both your contributions and all the earnings are completely tax-free.

Who it’s good for: If you believe you’ll be in a higher tax bracket in retirement than you are now, or if you like the idea of knowing your retirement withdrawals will be tax-free. Younger individuals early in their careers often find Roth 401(k)s appealing.

Important Note on Employer Match: Regardless of whether you choose a Traditional or Roth 401(k), any employer contributions will always go into your account on a pre-tax basis. This means when you withdraw the employer match portion in retirement, it will be taxed.

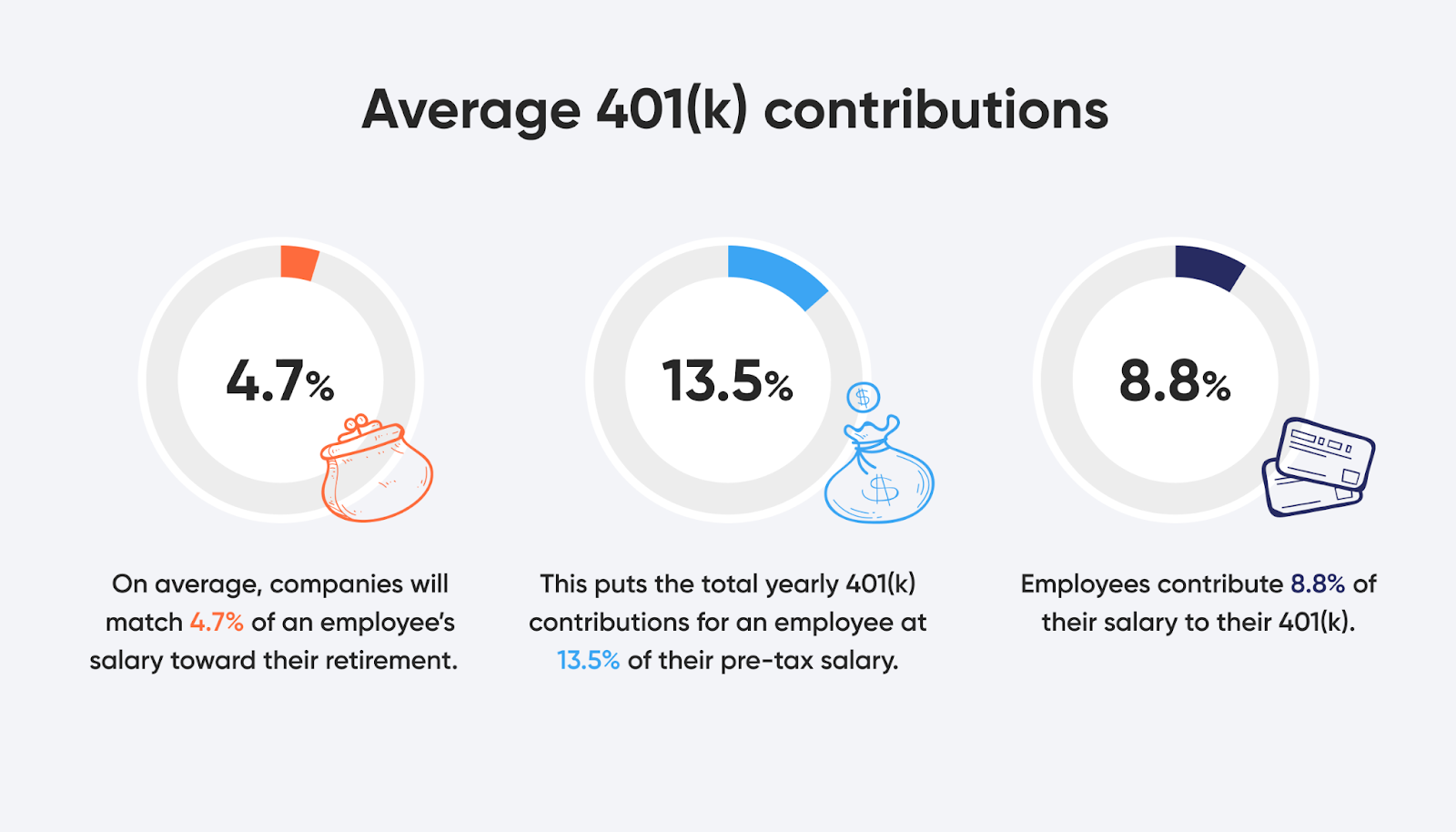

The Golden Ticket: Understanding Your Employer Match

This is arguably the most exciting part of a 401(k) plan and something you absolutely do not want to miss out on. An employer match is essentially free money that your company contributes to your retirement account, based on how much you contribute.

Think of it like this: if you put a certain amount into your 401(k), your employer agrees to put in an additional amount. It’s a benefit designed to encourage you to save for retirement.

How Does an Employer Match Work? Common Scenarios

Employer match formulas can vary, but here are some common examples:

-

Percentage Match up to a Certain Limit:

- Example: "We’ll match 50% of your contributions, up to 6% of your salary."

- What it means: If you earn $60,000 a year and contribute 6% ($3,600), your employer will contribute 50% of that $3,600, which is $1,800. So, you put in $3,600, and your employer adds another $1,800! That’s an instant 50% return on your contribution, just from the match.

- Key takeaway: To get the full match, you need to contribute at least 6% of your salary in this scenario.

-

Dollar-for-Dollar Match up to a Certain Limit:

- Example: "We’ll match 100% of your contributions, up to 3% of your salary."

- What it means: If you earn $60,000 a year and contribute 3% ($1,800), your employer will also contribute $1,800. You put in $1,800, and your employer adds another $1,800!

- Key takeaway: This is an even better deal, effectively doubling your initial contribution up to the limit.

-

Tiered or Discretionary Match:

- Some companies might offer different match percentages based on your years of service, or they might offer a "discretionary" match that changes year to year based on company performance.

Why You MUST Maximize Your Employer Match

This cannot be stressed enough: contributing enough to get your full employer match is the absolute minimum you should aim for in your 401(k).

- It’s Free Money: It’s literally extra compensation that your employer is offering. If you don’t contribute enough to get the full match, you are leaving money on the table.

- Instant Return: Where else can you get an immediate 50% or 100% return on your investment? This match instantly boosts your savings from day one.

- Compounding Power: That "free money" from your employer also starts growing and earning returns over time, thanks to the power of compound interest. A small amount today can become a significant sum over decades.

Action Item: Find out your company’s 401(k) match policy. It’s usually in your employee handbook, on your HR portal, or you can ask your HR department. Once you know, make it your top priority to contribute at least enough to get every penny of that match.

Unlocking Your Match: The Vesting Schedule

While the employer match is fantastic, there’s one more important concept you need to understand: vesting. Vesting refers to the amount of time you need to work for your employer before their contributions to your 401(k) officially become yours to keep.

Think of it like this: your employer’s contributions are "loaned" to you, and you "earn" ownership of them over time.

Common Vesting Schedules:

-

Cliff Vesting:

- How it works: You become 100% vested (meaning you own all the employer contributions) after a specific period of employment, often 1 to 3 years. If you leave before that "cliff" date, you forfeit all of the employer’s contributions.

- Example: A 3-year cliff vesting schedule means if you leave after 2 years and 11 months, you get none of the employer’s contributions. If you leave after 3 years, you get 100% of them.

-

Graded Vesting:

- How it works: You gradually become vested over a period of years, typically 2 to 6 years. You earn a percentage of ownership each year.

- Example: A 2-6 year graded vesting schedule might look like this:

- After 2 years: 20% vested

- After 3 years: 40% vested

- After 4 years: 60% vested

- After 5 years: 80% vested

- After 6 years: 100% vested

- If you leave after 4 years in this example, you would get to keep 60% of your employer’s contributions.

Why Vesting Matters:

- Job Changes: If you plan to change jobs, understanding your vesting schedule is crucial. You might want to time your departure to ensure you’re fully vested and don’t leave any employer match money behind.

- Long-Term View: Vesting is another reason why staying with an employer for a reasonable amount of time can be financially rewarding.

Important Note: Your own contributions to your 401(k) are always 100% vested immediately. You always own your own money. Vesting only applies to the money your employer contributes.

How Much Can You Contribute? (And Why You Should Aim High)

The IRS sets annual limits on how much you can contribute to your 401(k) each year. These limits can change, so it’s good to check the most current figures (they are typically announced in the fall for the following year).

For example, for 2024, the contribution limit for employees is $23,000.

The Power of Catch-Up Contributions

If you’re aged 50 or older, the IRS allows you to contribute an additional amount each year, known as "catch-up contributions." For 2024, this additional amount is $7,500, bringing the total potential contribution for those 50 and over to $30,500. This is designed to help those closer to retirement boost their savings.

Beyond the Match: The Power of Compounding

While getting the full employer match is step one, it shouldn’t be your only goal. If you can afford it, try to contribute more than just the match amount.

Why? Compound interest. This is the magic of earning returns on your initial investment and on the accumulated interest from previous periods.

- Example: Let’s say you contribute $5,000 annually and earn an average 7% return.

- After 10 years, your $50,000 in contributions could be worth over $70,000.

- After 30 years, that same $5,000 annual contribution could grow to over $500,000!

- Now, imagine if your employer match also contributed an extra $2,500 each year. Your total annual contribution would be $7,500, and your 30-year total could soar past $750,000.

The earlier you start and the more you contribute, the more time your money has to grow exponentially.

Making Your Money Work: Investment Options Within Your 401(k)

Your 401(k) isn’t just a savings account; it’s an investment vehicle. The money you contribute is used to buy various investment products, primarily mutual funds or exchange-traded funds (ETFs). Your employer’s plan will offer a selection of these.

Don’t just pick the default option! Taking a few minutes to understand your choices can significantly impact your retirement nest egg.

Common Investment Options You’ll See:

- Target-Date Funds: These are often the default option and a good choice for many beginners. A target-date fund is designed to simplify investing by automatically adjusting its asset allocation over time. For example, a "2050 Target-Date Fund" will start with a more aggressive mix (more stocks) and gradually become more conservative (more bonds) as you approach the year 2050.

- Index Funds: These funds aim to mimic the performance of a specific market index, like the S&P 500 (which tracks 500 of the largest U.S. companies). They are typically low-cost and offer broad market exposure.

- Mutual Funds: These are professionally managed portfolios that pool money from many investors to buy stocks, bonds, and other securities. They come in various types (e.g., large-cap, small-cap, international, bond funds) and have different risk levels and fees.

- Company Stock (Caution!): Some plans allow you to invest in your own company’s stock. While it might seem appealing, be cautious about putting too much of your retirement savings into a single company’s stock, especially your employer’s. It creates a "double risk" – if your company struggles, you could lose your job and a significant portion of your retirement savings. Diversification is key!

Understanding Risk Tolerance and Diversification

- Risk Tolerance: How comfortable are you with the ups and downs of the market? Younger investors with a long time horizon usually can afford to take on more risk (more stocks), as they have time to recover from market downturns. Older investors closer to retirement might prefer less risk (more bonds).

- Diversification: Don’t put all your eggs in one basket! A well-diversified portfolio means spreading your investments across different types of assets, industries, and geographies. This helps reduce risk. For example, instead of just investing in U.S. stocks, consider adding international stocks and bonds.

Action Item: Log into your 401(k) plan’s website and explore the investment options. If you’re unsure, a target-date fund that aligns with your expected retirement year is a solid starting point. As you learn more, you can adjust your strategy.

Managing Your 401(k): Key Steps to Success

Once you’ve enrolled and set up your contributions, managing your 401(k) isn’t a "set it and forget it" task forever, but it also doesn’t require daily attention. Here are the key steps to keep your 401(k) on track:

- Enroll Immediately (or as soon as eligible): Don’t delay! Even if you can only contribute a small amount initially, just get started. Many companies have an auto-enrollment feature, but always double-check.

- Set Your Contribution Amount: Aim for at least the employer match. If possible, gradually increase your contribution percentage each year, especially when you get a raise. Many financial advisors recommend saving 10-15% of your income for retirement (including your employer’s contributions).

- Choose Your Investments Wisely: As discussed, don’t just stick with the default if it doesn’t align with your risk tolerance or goals. Review the available funds and make informed choices.

- Review Regularly (Annually):

- Check Performance: How are your investments doing?

- Rebalance: Over time, your asset allocation might drift. If your stocks have performed exceptionally well, they might now represent a larger percentage of your portfolio than you intended. Rebalancing means selling some of the overperforming assets and buying more of the underperforming ones to get back to your desired allocation.

- Update Beneficiaries: Make sure the people you want to inherit your 401(k) are listed correctly. This is crucial!

- Check Contribution Limits: Ensure you’re not exceeding the annual IRS limits.

- Understand Fees: All investments come with fees. While 401(k) fees are generally lower than some other investment options, it’s good to be aware of them. Look for "expense ratios" on your fund choices – lower is generally better, as fees eat into your returns over time. Your plan administrator should provide a fee disclosure statement.

- Consider Consolidating Old 401(k)s: If you’ve changed jobs, you might have old 401(k) accounts. You typically have a few options:

- Leave it with the old employer (if the balance is high enough).

- Roll it over into your new employer’s 401(k).

- Roll it over into an Individual Retirement Account (IRA).

- Cash it out (generally a bad idea due to taxes and penalties). Rolling over into an IRA often gives you more investment options and control.

Beyond the 401(k): Other Retirement Savings Options

While your 401(k) is a fantastic starting point, it’s not the only tool in the retirement planning toolbox. Once you’ve maxed out your employer match (and ideally, your own 401(k) contributions), consider these:

- Individual Retirement Accounts (IRAs): Both Traditional and Roth IRAs offer similar tax advantages to 401(k)s but are set up by you directly with a financial institution, not through an employer. They offer a wider range of investment choices.

- Health Savings Accounts (HSAs): If you have a high-deductible health plan, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Many people use HSAs as a supplemental retirement account, especially for future healthcare costs.

- Taxable Brokerage Accounts: After maxing out all your tax-advantaged accounts, you can invest in a standard brokerage account. While these don’t offer special tax breaks, they provide ultimate flexibility.

Conclusion: Take Control of Your Retirement Today!

Your 401(k) is more than just a benefit; it’s a powerful engine for building long-term wealth and securing your financial independence in retirement. Understanding how it works, especially the critical role of the employer match, is the first step towards a brighter financial future.

Here’s your action plan:

- Find out your employer’s 401(k) match policy.

- Adjust your contributions to at least get the full match. Don’t leave free money on the table!

- Review your investment options and choose funds that align with your risk tolerance and goals.

- Consider increasing your contributions beyond the match if your budget allows.

- Regularly review and adjust your plan as your life and financial situation evolve.

Starting now, even with small steps, will make a massive difference thanks to the incredible power of time and compound interest. Don’t wait – your future self will thank you!

Disclaimer: This article provides general information and is not financial advice. Retirement planning and investment decisions should be made in consultation with a qualified financial advisor, taking into account your individual financial situation, goals, and risk tolerance. Tax laws and contribution limits are subject to change by the IRS.

Plans Explained: Your Ultimate Guide to Maximizing Employer Match and Securing Your Retirement")

Post Comment